The United States taxes its citizens and residents on their worldwide income.

Accordingly, the U.S. Internal Revenue Code requires U.S. taxpayers whose interests in foreign financial accounts exceed certain thresholds to report those interests in foreign financial assets on Form 8938, Report of Specified Foreign Financial Assets, filed with their annual U.S. income tax return.

The U.S. Bank Secrecy Act requires U.S. taxpayers whose interests in foreign financial accounts exceeds $10,000 at any time during the calendar year to file FinCEN Form 114, Report of Foreign Bank and Financial Accounts, (“FBAR”), for that calendar year.

Form 8938 and FBARs report much the same information. Reportable information includes the name and address of the financial institution, the account number, and the high balance of the account for the calendar year.

Significant penalties may be assessed for failure to file Form 8938. More importantly, the assessment statute of limitations as to a tax return—the entire tax return, not just the penalty for failure to file an information return—is suspended until Forms 8938 and like information returns due from the taxpayer have been filed.

A separate article addresses FBARs.

Who Must File Form 8938?

An unmarried individual resident of the United States must file Form 8938 if his aggregate balance of foreign financial assets exceeds $75,000 on any day of the year, or $50,000 on the last day of the year. A married couple resident of the United States who file a joint income tax return must file Form 8938 if their aggregate balance of foreign financial assets exceeds $150,000 on any day of the year, or $100,000 on the last day of the tax year.

An unmarried individual nonresident of the United States must file Form 8938 if his aggregate balance of foreign financial assets exceeds $300,000 on any day of the year, or $200,000 on the last day of the year. A married couple resident of the United States who file a joint income tax return must file Form 8938 if their aggregate balance of foreign financial assets exceeds $600,000 on any day of the year, or $400,000 on the last day of the tax year.

“Foreign financial asset” includes:

- Financial accounts maintained by a foreign financial institution; and

- The following foreign financial assets if they are held for investment

and not held in an account maintained by a financial institution:

- Stock or securities issued by someone that is not a U.S. person;

- Any interest in a foreign entity; and

- Any financial instrument contract that has an issuer or counterparty that is not a U.S. person.

A financial asset is a “foreign” financial asset is maintained with a foreign financial institution. It excludes a financial institution maintained with a U.S. office or branch of a foreign financial institution.

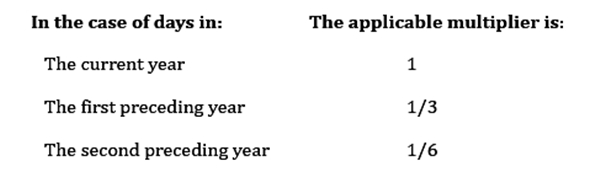

A “U.S. person” is a citizen or resident of the U.S., or a domestic (U.S.-based) corporation, partnership, estate, or trust. “Resident of the U.S.” means a lawful permanent resident of the U.S. (“green card” holder), or an individual who satisfies the substantial presence test. An individual satisfies the substantial presence with respect to any calendar year (hereinafter in this subsection referred to as the "current year") if:

(1) such individual was present in the United States on at least 31 days during the calendar year, and

(2) the sum of the number of days on which such individual was present in the United States during the current year and the 2 preceding calendar years (when multiplied by the applicable multiplier determined under the following table) equals or exceeds 183 days:

There are exceptions to the substantial presence test. For example, an individual shall not be treated as meeting the substantial presence test with respect to any current year if:

(1) such individual is present in the United States on fewer than 183 days during the current year, and

(2) it is established that for the current year such individual has a “tax home” in a foreign country and has a closer connection to such foreign country than to the United States.

Consequences for Failure to File Form 8938

A U.S. person files Form 8938 with his U.S. income tax return. A taxpayer is subject to a $10,000 penalty for failure to file Form 8938. The Form 8938 filing requirement applies to U.S. persons’ tax years beginning after December 11, 2011.

The assessment statute of limitations with respect to Form 8938 is three years. But it does not start running until the Form 8938 in question is filed. In other words, there is no assessment statute of limitations on the penalty for failure to file Form 8938.

Significantly, Internal Revenue Code (“IRC”) § 6501(c)(8)(A) provides that the failure to file Form 8938 or like information return suspends the assessment statute of limitations, not only as to the penalty for failure to file the information return, but as to the taxpayer’s entire income tax return for that year.

Reasonable Cause Penalty Relief

If the IRS proposes or assesses a penalty for failure to file Form 8938, the taxpayer should consider requesting reasonable cause penalty relief. The classic reasonable cause scenario is a taxpayer who exercised reasonable care but due to factors beyond his control was unable to comply with the law. For example, a taxpayer who was advised by a tax professional that he need not report his interest in foreign financial assets to the IRS has reasonable cause for not filing Form 8938. A taxpayer could also have reasonable cause for failing to file Form 8938 if the taxpayer’s tax advisor knew or should have known of the taxpayer’s interest in a foreign corporation, and failed to advise the taxpayer to file Form 8938, where the taxpayer did not otherwise know that he was required to file Form 8938.

Conclusion

A taxpayer with one or more delinquent Forms 8938 should file them as soon as possible.

Stephen J. Dunn is a tax attorney in Troy, Michigan. He is the author of the treatise Foreign Accounts Compliance (Thomson Reuters 2017) and Foreign Accounts Compliance Blog. He is also an adjunct professor at Michigan State University College of Law.

© 2026 Newsmax Finance. All rights reserved.