“Rising interest rates slow the housing market as people buy payments, not houses, and rising rates mean higher payments.”

The housing recovery is ultimately a story of the “real” employment situation. With roughly a quarter of the home buying cohort unemployed and living at home with their parents, the option to buy simply is not available. Another large chunk of that group are employed but at the lower end of the pay scale which pushes them to rent due to budgetary considerations and an inability to qualify for a mortgage.

Even after a “decade of recovery,” the full-time employment-to-population ratios remain well below levels normally associated with a strong economy, and wage growth remains stagnant. Both of which makes home affordability an issue.

Despite much of the media rhetoric to the contrary, I have warned repeatedly that rising rates would negatively impact the housing market which was still being supported by low interest rates.

The mistake that mainstream analysts made was in the assumption that the recent increases in real estate prices were largely driven by first time home buyers creating an organic market. The reality, however, has been that market increases were being driven by speculators in the “buy to rent” game. As I noted previously:

“As the “Buy-to-Rent” game drives prices of homes higher, it reduces inventory and increases rental rates. This in turn prices out “first-time home buyers” who would become longer-term homeowners, hence the low rates of homeownership rates noted above. The chart below shows the number of homes that are renter-occupied versus the seasonally adjusted homeownership rate.”

“Speculators have flooded the market with a majority of the properties being paid for in cash and then turned into rentals. This activity drives the prices of homes higher, reduces inventory and increases rental rates which prices ‘first-time homebuyers’ out of the market.

The recent rise in the home-ownership rate, and subsequent decline in renter-occupied housing, may an early sign of rental investors, aka hedge funds, beginning to exit the market. If rates rise further, raising borrowing costs, there could be a ‘rush for the exits’ as the herd of speculative buyers turn into mass sellers. If there isn’t a large enough pool of qualified buyers to absorb the inventory, there will be a sharp reversion in prices.”

You can see that a bulk of the real estate activity has occurred at the price levels of homes that make the best rental properties – between $200,000 and $400,000.

Importantly, you can see activity has dropped sharply over the course of the last couple of months. This is particularly the case at the very high-end and very low-end of the spectrum.

The latest data on existing and new home sales, permits, and completions show that we have likely seen the peak from the bounce in housing activity that started in 2010. It is important to remember, as we have discussed previously, that there are only a certain number of individuals that, at any given time, are actively seeking to ‘buy’ or ‘sell’ a home in the market. Furthermore, individuals buy “payments,” not “houses,” so artificially suppressed interest rates are only half of the payment equation. When home prices increase to levels that begin to price buyers out of the market – activity will slow.

The chart below is our Total Housing Activity Index which simply combines the 4-primary components of the housing market cycle – permits, completions, and sales of new and existing homes.

You will notice the last time the activity index broke is rising trend, the subsequent decline was not healthy. More importantly, both the current, and previous, “housing bubble” preceded the peak in household net worth.

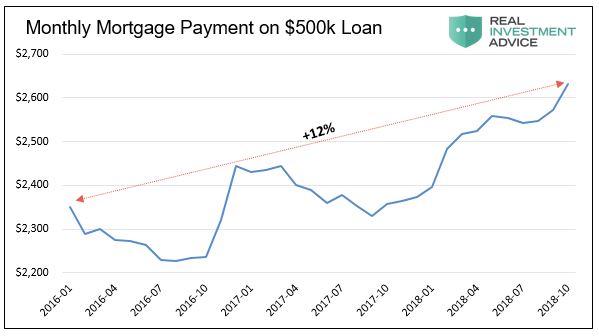

In both cases, the “pin that pricked the bubble” was interest rates. As shown below, when mortgage rates rise housing activity slows as “people buy payments” rather than houses. This is because higher rates have two immediate impacts on the housing market:

- The monthly payment rises to a level that buyers can’t afford, or;

- Buyers stop their activity to “wait and see” if rates come back down again.

The monthly mortgage payment required for a loan has risen about 12% over the last three years as mortgage rates rose approximately 1%. The simply put houses out of reach for a vast majority of Americans already living from one paycheck to the next.

As a result, and shown below, the annual growth rate of housing activity is back into negative territory.

However, it is really how many of those “permits” turn into “completions” that matter. Currently, that ratio is sending an important warning which is suggesting more troubles ahead for the housing market as “permits” are being pulled due to lack of demand.

At The Margin

Another “Damocles Sword” hanging over the mortgage industry is that rising interest rates will continue to kill the “refinance market.” Banks and mortgage-related companies have made huge profits over the last couple of decades as homeowners serially refinanced their homes to take out cash and refinance at a lower mortgage rate. That activity has largely ceased as a result of higher rates. We are now seeing default risk rise as adjustable rate credit lines on home equity loans begin to exceed homeowners ability to service the debt.

Furthermore, individuals were previously able to sell their existing home and “upgrade” to a newer or larger home. That upgrade was afforded by extremely low interest rates. Now, as rates rise, the “trade up” activity will greatly diminish as individuals become locked into their existing homes.

Housing is always a function of what happens at the “margins” with the activity contained to those actively searching to buy a house versus those willing, or able, to sell. But in order for MOST individuals to engage in the housing market, they need a mortgage to do so. As rates rise, that activity slows.

There is no argument that housing has indeed improved from the depths of the housing crash in 2010. However, that recovery still remains at very weak historical levels and the majority of drivers used to get it this point have begun to fade. Furthermore, and most importantly, much of the recent analysis assumes this has been a natural, and organic, recovery.

Nothing could be further from the truth as analysts have somehow forgotten the trillions of dollars, and regulatory support, infused to generate that recovery. We must also remember that record low mortgage rates driven by Fed purchases of Mortgages Backed Securities (MBS) played a large role in the recovery.

Homebuilder sentiment has gone well beyond the actual level of activity. The recent turn lower is bringing that over-confidence back to reality and with that expect to see a decline in new permits and likely rise in the unemployment rate of those involved in the housing sector.

For the housing market, the recent rise in interest rates is extremely important. There are many hopes pinned on housing activity continuing to foster the domestic economic recovery. If rates do indeed pop the current housing “bubble,” the entire economic recovery thesis will be called into question.

While the Fed has repeatedly noted the strength of the economy as a central underpinning for continuing to hike rates and tighten monetary policy, it is quite likely the damage from rising rates has already been done. Such was noted yesterday when Fed Chair Jerome Powell reversed his position on hiking rates and changed the language to suggest they were close to finished.

But the Fed’s change of tone may just be “too little, too late” as the negative impacts of increased borrowing costs with respect to both auto loans and housing have already become evident. It is only a function of time until the broader economic indicators feel the pinch.

Lance Roberts is a chief portfolio strategist and economist for Clarity Financial. He is also the host of "Street Talk with Lance Roberts," chief editor of "The X-Factor" Investment Newsletter and the Streettalklive daily blog. Follow Lance on Facebook, Twitter and LinkedIn.